I've been asked a lot about a hobby I take part in called churning. I thought I'd write up a post that explains what it is, how I got into it, and how much value it can provide.

How I got into churning

Completely unaware of American finances, I moved from Italy to Los Angeles, California in 2014. I was coming into my freshman year of college, and moving to the United States - it was a time of extreme change and shock, both from a cultural and personal perspective. I didn't know much about finance, banking, or credit in the US, but I knew I wanted to be financially responsible and independent. I started by opening an account at my university's credit union and used it for my direct deposit from my on-campus job. Near the end of the year I thought I should get started on building out my credit - I didn't know much about credit scores, so I did a quick search for "college credit cards" and the Capital One QuickSilver popped up. Thinking nothing of it, I applied and got immediately approved. I didn't look at the bonus, requirements, or interest rate - I just knew I wanted a credit card, and that I wouldn't ever carry a balance, so what did it matter.

I didn't know it at the time but the bonus attached was get $100 after spending $500 in the first 3 months. I easily spent that and got an email confirming that I got the bonus. I didn't even realize this was possible - I cashed it out and received a check in the mail for $100 and some odd change. This was a huge amount of "free" money for a college freshman.

I was immediately hooked.

What is the hobby?

I started doing my research - would opening a lot of cards "hurt" me financially? Were there any risks involved? Could I close this card and reopen it? I stumbled across a subreddit, /r/churning, after reading a few blogs. It was still fairly small at the time, no more than 20,000 subscribers. These were people talking about manufactured spending, having millions of miles, and never paying for a flight. They would expend a minimal amount of effort and fly first class to Hawaii, with all the luxuries that came with that. I dove in head first - I consumed every wiki article, trying to acquaint myself with what was really going on.

At its core, churning is taking advantage of credit cards, bank accounts, travel rewards programs, and various other promotions. That's it - it comes down to doing your research about the best available offers and maximizing your potential value.

The logic behind the lucrative rewards, as far as I can tell, is the fact that most people won't open up 50 credit cards. The average consumer will look for a credit card, maybe research the current best offer, then sign up for it and keep it for 20 years. The banks and airlines can afford a really high initial investment in the form of miles/cash because they assume the consumer will either A) carry a balance and pay interest or B) use the card for such a long time that the interchange fees will dwarf the initial bonus.

Take the Chase Sapphire Reserve when it originally came out - the 100k UR sign up bonus + other benefits was easily worth $1,500 in total. These benefits were handed over pretty much as soon as you got the card and met the bonus.

Why does this exist? How do the banks make money?

It seemed a little crazy that I could get a free $1,500 by paying for my rent on my credit card instead of directly from my bank account. The reason this works and isn't a scam is that most people do not take full advantage of these offers - some people can't financially support the amount of required spend, some aren't fiscally responsible, and others just don't want to expend the effort.

-

American credit card debt hit $1,027,000,000,000 in March 2018, according to the federal reserve1.

-

38% of US households have revolving credit card debt (debt they are carrying month-over-month, and paying interest on)

-

The average American has 3.1 credit cards with $6,354 of debt2.

These statistics paint a scary picture as a consumer but are extremely lucrative for the banks.

The banks make money primarily in two ways:

-

The customer carries a balance month-over-month, and the bank collects interest. The interest rate, as of this writing, can be as high as 25.99% - this is exorbitant, and where most people fall into a vicious payment cycle, only ever paying off last months accrued interest, and never decreasing the principle.

-

Interchange fees. These are the fees that are charged to vendors and stores so that they can accept the payment method (Visa, Mastercard, Amex, etc). Sometimes the company that ends up with the interchange fee isn't the bank, but rather the payment processor, but that's beyond the scope of a churning primer.

Over 50% of Americans carry a monthly balance on their credit cards. This is an extremely lucrative model for the banks - most people are aren't taking full advantage of their benefits, and they're paying up to 25.99% of their balance every month.

On top of interest, banks charge interchange fees ranging from 0.75% to 3% of the total purchase. This means that even if you're a churner the banks will recoup some of their losses - that $5k initial spend requirement will net Amex $5,000 * 0.03, or $150 in interchange fees. Not enough to recoup a $1,000+ initial sign on bonus, but enough that if it's sustained over time they'll end up net positive.

Credit

Churning will definitely affect your credit score, and, if not done properly, will almost certainly hurt it. You are applying for multiple lines of credit across a broad range of financial institutions - this is not normally a good sign. You'll need to know how to properly handle your own finances and how to make sure that your behavior does not look like that of a high risk individuals'.

First, it's important to note that you don't have one credit score. There are multiple credit bureaus, and each of these bureaus have different credit scores (for instance, your score when applying for a mortgage or a car loan is going to be different than when applying for a bank account that does a hard pull). However, people commonly talk about the FICO8 credit score, from one the main 3 bureaus, Experian, Equifax, and Transunion.

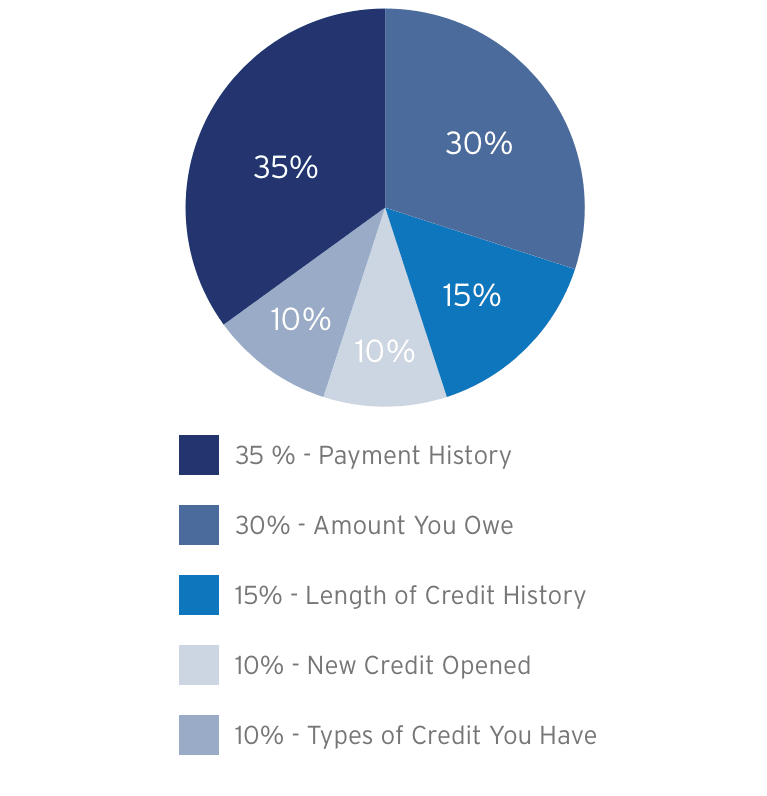

This credit score is broken down in the following categories and weights:

- 10% - Types of Credit

- 10% - New Credit Opened

- 15% - Average Age of Accounts

- 30% - Amount Owed

- 35% - Payment History

Credit percents

Credit score breakdown

If you see here the lion's share of your credit score is going to be the amount you owe at the end of each month, and your history in paying that off. If you're doing churning right those will be $0 and 100% ontime payments, respectively.

Where churning will hurt you is in the average age of accounts and new credit opened. Every new card will lower your average age of accounts - typically this isn't that big of an issue though. I had ~20 hard pulls on my credit report with 42 cards opened in the last 24 months and I was sitting at a 786. The most important part of the hobby is to make sure to never pay a cent of interest and to never forget a payment.

In the long run churning will actually help - the average age of accounts will be backloaded if you open a large amount of cards at once, which means that if you open another card in 5 years its effect will be amortized by the sheer number of cards opened 5 years ago.

Churning will also help the last category, types of accounts. Most credit score estimators say you need ~20 accounts opened to max out the potential value from the last category.

Advanced Churning and Risks

Once you feel like you have a good grasp on the game and are generally in tune with what's happening in the credit world you can try diving into deeper topics. The two most lucrative are going to be A) Manufactured spending and B) Business bonuses.

You can register a business as a sole proprietorship - even if you have no or little income. You can create a sole proprietorship for a dog walking business, a baby sitting service, or just a general consulting company (which is what I did). This opens up a whole new world of cards and bonuses.

Manufactured spending is the art of cycling through your credit without actually spending any money. This is probably the most "dangerous" part of churning - this looks a lot like money laundering, but is completely legal. An analogy would be like washing fake blood off the front of your car in broad daylight. A little weird, and the cops might get called, but you didn't do anything wrong. MS'ing looks a lot like money laundering, and in fact uses a lot of the same techniques.

Manufactured spending is also the most volatile - there's no generally accepted way of MSing, new avenues open and close every month. It relies a lot more on one-off deals.

The gold standard for years was money orders - you could go to Walmart and buy $10,000 in gift cards when a promotion was going on for no fees, then go to any USPS and use to Vanilla gift cards to buy money orders. The fee for this about $1.25 per $1000. The money orders could then be directly deposited in your bank account, with which you pay off the original credit card. This meant your overhead was $12.50 per 10,000 miles/points. A round trip to Europe is (currently) 45,000 miles on AA, so this would just cost you $56. Unfortunately this was pretty much shutdown in late 2016 when USPS stopped taking gift cards.

There are much more complicated ways to MS, and it's difficult to write a guide around. Once you have an eye for the game you can spot these opportunities pretty quickly - finding a store that'll reimburse costs to any card, not just the original card that was used, buying cash from the US treasury with a credit card, 100% value rebates, etc. These are usually short lived and get hit pretty hard since they can be so rewarding.

Bank defenses

Over the past 3 years banks have become much more aggressive at trying to find the people gaming the system - an individual can easily take over $10,000 in benefits from these companies over the period of a couple of years if they play their cards right. Chase introduced 5/24 (they won't approve you for any more cards if you've gotten 5 cards in the last 24 months from any issuer), Amex has the once per lifetime rule, and Citi shut down the AA mailers code reuse. Amex even started clawing back bonuses if your purchases included gift cards or anything that could be construed as manufactured spending.

The hobby is definitely not dead but the walls are closing in more and more every year. Don't let anyone tell you that churning is dead, though - there are simply too many people subsidizing the hobby by paying interest and being fiscally irresponsible.

Getting started

I'm not going to make recommendations on where to start or how to do this - chances are by the time you're reading this, the advice of the day will be outdated, and some bonuses won't exist anymore. There are a ton of great guides on /r/churning, with flowcharts and easy to understand principles. You'll need to decide on whether you want to focus on miles, hotel points, or cash, and on how many people you'll be doing this with (if you have a significant other it changes the dynamic quite a bit! Look into "player 2 mode" for churning!).

Personal stats

I'm now a moderator of /r/churning, hit a grand total of a million miles earned, and haven't paid full price for a flight since 2015. I have status at most hotels and all the major US airlines, and have access to at least one lounge every time I fly. I've been consistently doubling the number of flights I take per year (I'm on track for 36 in 2018, while being a full time student). I've been to 20 countries by the time I was 21. This is while having a negative net worth (student loans) and only 3 months of income per year.

The real value from this comes from the fact that I'm still in college - this allows me to travel in a way that's way above my means, in a type of luxury that I could never afford.

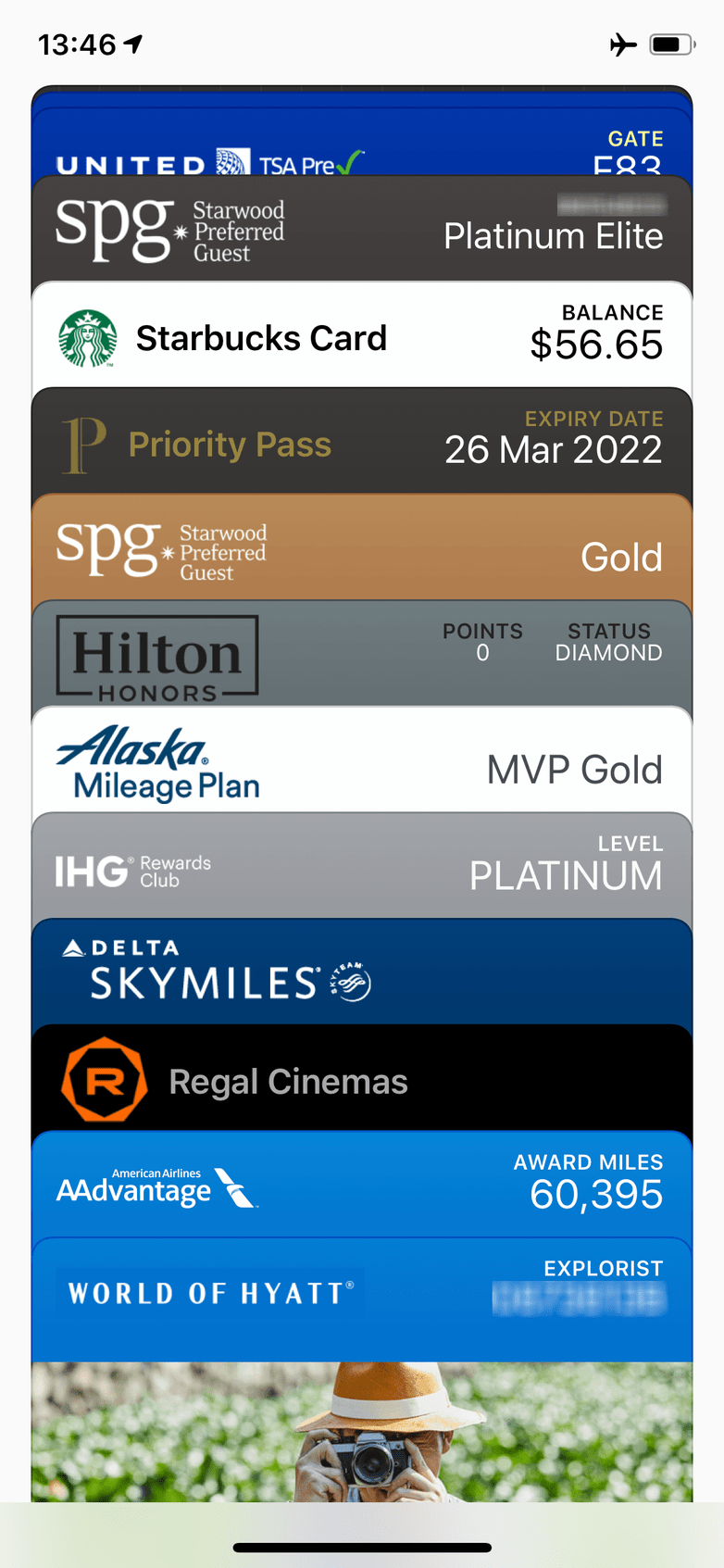

My wallet status

Screenshot of my iOS wallet with some of my frequent traveler cards