American Airlines is an e-currency company that happens to own some planes. (at least when looking purely at their profit)

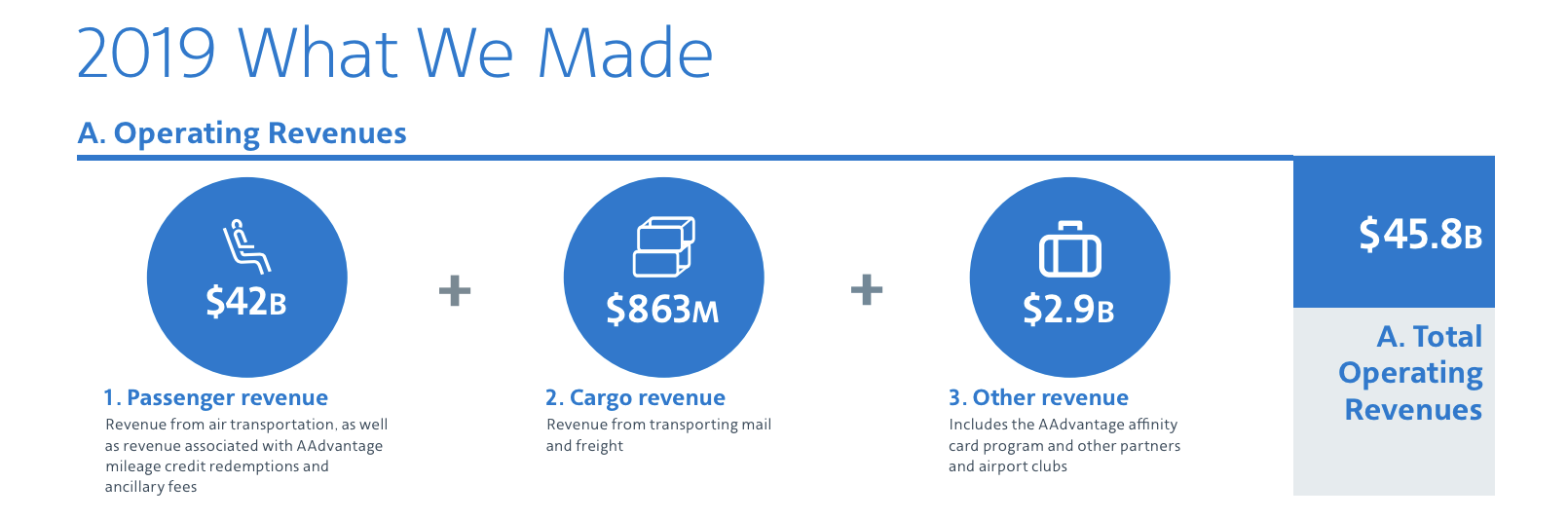

American Airlines (AAL) is the largest airline in the world, as measured by number of passengers carried, by fleet size and by scheduled passenger-kilometers flown. It has $60 billion worth of assets, on $34 billion of debt, with $46 billion in annual revenue and $1.7 billion of GAAP net income (2019)1.

Earnings

AA is close to break even when accounting purely for their flight operations and income. They made $42 billion in passenger revenue and $900 million in cargo revenue, but spent $42.7 billion to get there.

What actually made them profitable, in 2019, was the sale of airline miles to banks. They made $2.9 billion selling miles, which was almost pure profit for them.

You can read through their 10-Q SEC filing here.

Of note:

Mileage credits can be redeemed at any time and do not expire as long as that AAdvantage member has any type of qualifying activity at least every 18 months. As of March 31, 2020 , our current loyalty program liability was $ 3.1 billion and represents our current estimate of revenue expected to be recognized in the next 12 months based on historical trends, with the balance reflected in long-term loyalty program liability expected to be recognized as revenue in periods thereafter. Given the inherent uncertainty of the current operating environment due to COVID-19, we will continue to monitor redemption patterns and may adjust our estimates in the future.

They list $3.1 billion in current mileage credit liabilities, which are liabilities that will be redeemed within the next year, and $5.8 billion in non current liabilities, or debts they expect to be paid back more than a year from now 2.

In fact, loyalty program participants often let their miles lapse and expire worthless - nearly 46% have at some point let it expire, according to this (non peer reviewed, online) study by Bankrate, while for AA specifically it seems closer to 20%.

AAdvantage

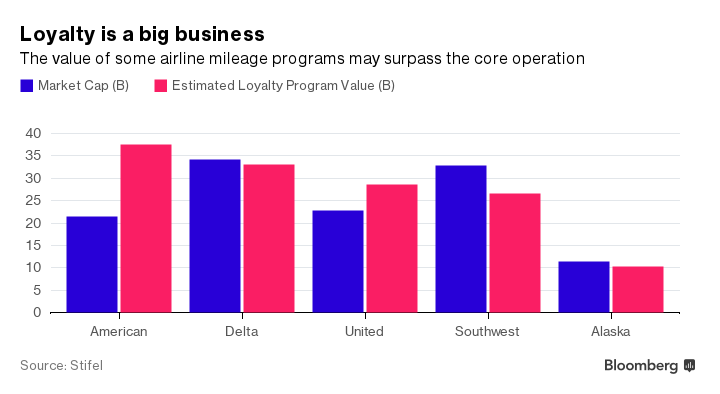

A 2017 report actually placed the value of AAdvantage, AALs loyalty program, at twice that of the actual flight operations. 3

Straight from that report:

As a refresher, here is the basic process behind the business of airlines selling miles to credit card companies. As a holder of an airline co-brand credit card, you earn miles based on your spend on the card. The credit card company - Chase, Citi, AmEx, etc... - needs to then purchase those miles from the airline in order to give them to you as your reward for spend. The card company purchases the miles from the airline for roughly 1.5c-2.25c per mile. For the purpose of this exercise, we'll assume it is sold at 1.75c. The airline makes an estimate as to what that mile will cost the airline when it is redeemed which is based on a number of factors including the rate at which the airline sells miles to other airlines for (should you choose to earn miles on American Airlines, for example, on a flight with Alaska Airlines). Let's assume that the cost of the mile is roughly 0.8c. This portion of the proceeds - the 0.8c, - is deferred onto the balance sheet as frequent flyer deferred revenue and recognized as the miles are redeemed (we estimate the liability is amortized over a roughly 24-28 month period). We assume that this margin flows through the income statement at a relatively high margin because (1) our discussions with loyalty program consultants and the airlines would suggest this, (2) the cost estimate of the mile reflects the fair value, to some degree, of the mile not the incremental cost, and (3) our margin estimate includes the benefit of any where from 15%-22% of miles sold not being redeemed (i.e. breakage/spoilage) and flowing through at 100% margin.

The remainder of the proceeds from the miles sold - the 1.75c minus the 0.8c, in this example - is referred to as the marketing component and is essentially the profit, or "mark-up" as some airlines call it, associated with selling miles for more than they cost the airline when redeemed. The marketing component revenue is not deferred and is recognized immediately and flows through Other revenue. We conservatively estimate this revenue stream at a 90% margin to account for some overhead associated with administering the program and minor costs associated with lounge access or bag fee waivers that certain cards provide.

AADV?

The only reason AAL has been profitable, recently, is due to it selling its virtual currency.

The market cap of AAL in 2017 was $21 billion - this report valued AAdvantage alone at $37.6 billion. A few analysts and investors have speculated that spinning AAdvantage out into its own company would value both companies more correctly, and potentially help AAL raise some much needed cash (AADV anyone?).